Apr

17

Superman is faster than a speeding bullet, more powerful than a locomotive, and able to leap tall buildings in a single bound. But he’s not invincible. Kryptonite weakens him. If he gets too close, that little glowing green rock will bring him down to his knees. Let me ask you a question. Does Superman hang around kryptonite or does he try to avoid it? It’s obvious: He avoids it. Just like the Man of Steel, you and I also have our own kryptonite — financially speaking. We all have stores that weaken our financial resolve and make us buy — think Costco, Best Buy, Apple, Zara, and Barnes & Noble. But instead of avoiding our kryptonite stores (like Superman would), we walk or click right into them, and convince ourselves that we’re just going to “look.” But we all know, when we get too close to our kryptonite, we get weakened and buy stuff we didn’t want to get. And the stores know this. They use sneaky Lex Luthor ploys to draw you in and make you buckle. But don’t fall for it. Instead, be like Superman: Know what your financial kryptonite is, recognize the tactics it uses to draw […]

Apr

10

Budgeting is 80% emotional and 20% numerical. In other words, 80% of your success with budgeting is based on your emotions, while only 20% is based on your numbers. Learning how to deal with fear, jealousy, and regret are the main components of budgeting you need to master. Sure, an app can crunch your numbers. But it can’t master your financial emotions for you. That’s your project. Once you nail the 80% — the financial emotions — you’ll look and treat money differently. And when your perspective shifts, something magical happens — you’ll become smarter with money and finally start to feel in control of your finances.

Mar

26

Tension is what makes us take action. It’s the urgency that we feel when we need to get something done. If there isn’t enough tension, we “push it off” and don’t do anything. With finances, for example, we feel tension when we see a larger than expected credit card bill or a line of credit that just keeps on going up. We know we need to change. But our first gut reaction is to run away from the tension — to get rid of it. So we bail ourselves out by consolidating our debts, refinancing our mortgages, or asking a wealthier family member for a loan. And the debt cycle continues because we got rid of the tension but never really changed our financial behaviors. Let me ask you: What if we didn’t seek to mute our tension, but ran towards it? In other words, instead of procrastinating, what if we: Started to save for unexpected expenses? Came up with a solid plan to pay off our debt? Figured out a way to get smart with our money? Seth Godin put it best when he said: “When you encounter the tension of now, caused by the urgency of action, veer […]

Mar

19

Mint, Quicken, Mvelopes, and YNAB are just a few budgeting apps out there. They’re all useless. Useless, if you’re not ready to change. All too often, we look for tech to solve our problems. That’s our starting point. Like if we find the right computer program or app, all our financial worries will go away. So we load all our data in and categorize for hours. Finally, we can see where it’s all going, look at some pie charts and graphs. But then we continue with our regular lives. Nothing changes. Know this: Your willingness, determination, and tension are the main ingredients when it comes to budgeting — not an app. Tech isn’t the solution. You are.

Mar

11

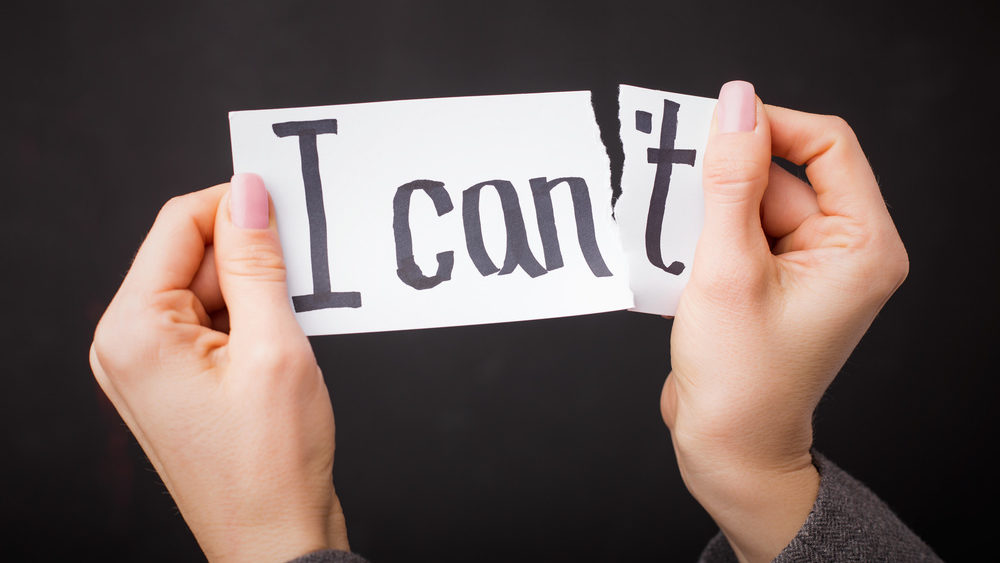

Here are some common things we say: I can’t lose weight. I can’t have supper with you tonight. I can’t get that project done on time. I can’t be happy. Here are some financial (and common) things we say: I can’t pay off my debt. I can’t save money. I can’t budget. I can’t make more money. I can’t, I can’t, I can’t. Does that sound familiar? We say “I can’t” to ourselves all the time. And in some weird way, it makes us feel better — like we become exempt from the trouble because we simply can’t do it. But you and I both know, “I can’t” is just an excuse. Really: I can’t = I won’t. Ouch, that doesn’t sound so good, right? Here’s an idea. Instead of I can’t, try “I can if…” Permit yourself to dig deeper. I can if _____________________________. (Go ahead, try it. Fill in the blank.) What would happen if you became a “can-if” person? Like everything is figureoutable. How would your world look? Could something so simple have a profound effect on your finances and your life? I know it does. Do you? Tell me in the comments below.

Feb

26

Most of us keep our finances to ourselves. Kinda like holding a deck of cards to our chest. I get it — we’re afraid what people think about us. Maybe they’ll think we’re a failure. Or worse, maybe they’ll see that we’re a fake. So, as a result, we end up alone in fear of our finances (and interestingly, you can have a spouse and still feel alone.) But what if there was a different way? What if there was a safe-bubble; a group of people who had the same struggles as you, and were all heading in a new direction? Like a community, or a tribe, that gives support and comradery. An openminded group that gives honest feedback, and collectively helps you, and you help them fix their finances. No judgment calls. Ever. What would that look like? How would that make you feel? If someone was holding out their hand and said “Hey! Let’s get out of this place. We’re all heading in a new direction. Hop on!” Would you take the leap? Let me know in the comments. I’m curious.

Feb

25

Here’s a list of common financial lingo you probably already know: Spreadsheet Forecast Cash-flow Debt repayment Surplus Retirement savings Unexpected expenses Equally as important, but not as well known, here’s a list of “uncommon” financial lingo: I have the power to change. I can. I will. I’m in charge today. I’m happy with what I got. I’m not going to compare myself with others. I deserve financial control. If you wanna take charge of your money, you have to understand the “uncommon” lingo in your heart. Your finances are dependant on it. It’s that simple. Now it’s your turn… What kinda financial lingo do you tell yourself? What would you like to change it to? Tell me in the comments below. I’m curious.

Feb

18

Does “taking control of your finances” sound impossible to you? Sure, you might be able to budget for a week or two, but after that, fuhgeddaboudit. C’mon, you’ll never stick to a budget. Right? Does that sound familiar? Listen carefully; you should know, it IS possible for you to master your money, once and for all. Lucky for you, I have an ancient secret that’ll give you Lance-Armstrong-like endurance for budgeting. (No steroids needed. I promise.) 💪 💪 💪 What’s the secret? The secret to money-mastery is in the Japanese concept: ShuHaRi. Initially, a martial art approach, ShuHaRi represents the three stages of learning (Shu, Ha, and Ri) that transforms a person from being a novice to a master. (Interestingly, in Japan they don’t talk about “ShuHaRi.” It’s just the way they’ve been learning for hundreds of years.) In a nutshell, here’s how it works: Step 1: Shu (obey) – In the beginning, you seek out a mentor. Mimic their methodologies — following directions to a tee. Just think of “wax on, wax off” in the Karate Kid. Step 2: Ha (digress) – Once you got the basics down cold, you start to branch out and collect other techniques from other mentors. […]

Feb

12

I’m not a coupon cutter — and probably will never be one. My wife, Yael, on the other hand, is the complete opposite. She always knows where to save 0.50¢ on English Cucumbers and a buck off a box of Cheerios. Yael is what I call a “micro-saver.” Don’t get me wrong; I think coupons and price matching are fantastic. I just wasn’t built like that. I’m more of a “macro-saver” (versus a “micro-saver”). In other words, I look at big ways to save money that don’t take a lot of time. And if you’re a macro-saver like me, today’s your lucky day. Below, I’ve put together my top 3 macro-saving tips, which could put thousands of dollars back into your wallet — without cutting a single coupon. 😉 Tip #1 ThriftBooks.com Thriftbooks connects you to discount wholesalers that’ll sell you a new or used book for a fraction of the retail price. Take Malcolm Gladwell’s, The Tipping Point, for example. In hardcover, Barnes and Nobels sell it for $18.98. At Thriftbooks, it’s $4.59 for a *like-new copy. (* My experience of like-new is that it’s really “like-new.”) In other words, you can buy four books for the price of […]

Feb

05

I believe: People can change. A rut is a temporary place to get you to the next level. Spouses can work together as a team. It’s never too late. Urgency makes things happen. Opening up is healthy. Not making a decision is making a decision. Taking control takes guts. Knowing is half of the battle. The other half is doing. and most importantly… You can nail this financial thing. What do you believe? Tell me in the comments below…

« Previous Page — Next Page »